There is a number that keeps appearing in earnings calls, infrastructure announcements, and government industrial strategies, and it keeps getting bigger. A hundred billion here. A quarter of a trillion there. The figures attached to AI investments have become so large and have been repeated so often that they no longer seem to elicit a reaction from most investors.

While on its face this massive expenditure could be taken as a sign of optimism, we have yet to find out whether these capital flows will result in a genuine productivity transformation or if it is simply the behaviour of empires that have run out of organic growth and are attempting to manufacture a new engine to replace the industries that are quietly stalling in the background.

From the railroads of the 1800s to the internet buildout of the 1990s, every major technology cycle produced a capex boom. In each case, enormous quantities of capital were deployed ahead of proven returns, and typically the infrastructure outlasted the investors who funded it with gains accruing to those who sold the “picks and shovels” rather than the owners of the infrastructure itself.

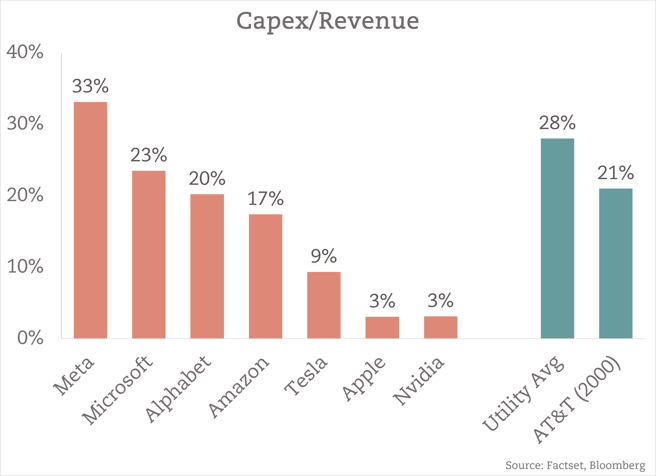

Training an AI model requires billions of dollars of GPU infrastructure before it can be deployed. The capital must be committed years in advance of any revenue, using projections about model capabilities, user demand, and competitive dynamics that are, at best, educated speculation. Robotics deployment, which is increasingly central to the AI commercialization story, means fleets of depreciating physical assets in the field, which are subject to maintenance cycles, and the operational complexity of any heavy machinery business. The industries AI is meant to transform (such as manufacturing, defense, health and energy) are already capital-intensive, and the AI layer does not make them less so. It just adds a further capital requirement on top.

Capital-intensive industries can be extraordinarily productive and profitable. But they operate on different economics than the asset light, zero-marginal cost models that many of these companies are historically used to. Returns will arrive later, are more sensitive to financing costs, and are far more exposed to the business cycle. A firm that borrowed cheaply in 2023 to build GPU clusters may be sitting on assets with very different economics in 2027, particularly if the models they were built to train have become outdated.

AI is being positioned as the answer to the slowing or stagnant economic growth that Western countries have experienced over the past few decades. However, the investment case is often not driven by neutral analysis of the technology and whether the potential productivity gains are of sufficient magnitude to justify the investment. In many cases, it is driven by the very companies whose growth problem AI is meant to solve and is encouraged by governments who are hoping for a “magic bullet” to get them out of their bleak fiscal situations. The spending is on such a scale that governments and companies can’t afford to acknowledge that this thesis might not hold.

In 2025, U.S. business investment expanded by nearly 6%, six times faster than in 2024¹. But nearly three-quarters of that growth was driven by AI-related investments, while most other areas remained weak. Strip out the data centres and GPU clusters, and the business environment looks considerably less optimistic. While this massive spending makes headline growth numbers looks good, it is masking the fact that the rest of the “real” economy is struggling and will likely face further issues as AI capex shrinks the pool of available capital that these businesses rely on to expand. With nearly all investment being channeled into just one area, the consequences of failure are high. When combined with the fact that the rest of the economy is in no position to cushion the blow if AI fails to live up to expectations, and the consequences become far worse.

This is the dynamic that should concern investors more than any specific technical risk. It is not that AI is useless, the technology is genuinely impressive and the productivity applications in specific domains are real. It is that the investment is driven at least in part by strategic necessity rather than purely by return on capital calculations.

There are scenarios in which the current AI investment wave looks like the electrification buildout. In the years following its discovery, vast amounts of speculative capital were deployed, leading to a period of destruction as the weaker players failed, followed eventually by productivity gains that more than justified the total investment even if some investors were wiped out along the way.

There are also scenarios in which it looks more like the telecom buildout of the 1990s where the underlying technology was real, but investment occurred at a scale and speed that could not be justified by the revenues that materialized, leading to write-downs, consolidation, and years of value destruction.

With so many unknowns surrounding how the AI revolution will unfold, it is important for investors to not fall into the camp of blind enthusiasm nor reflexive skepticism, but to take a pragmatic view that understands that the opportunities are real while acknowledging that the path will likely be more uneven and more cyclical than many are assuming. AI will produce meaningful winners, but not necessarily among the firms attracting the loudest narratives or the largest valuations today. Many of the biggest names at the peak of the DotCom bubble faded into irrelevance while companies like Google and Amazon, which were relatively unknown at the time, replaced them.

BOTTOM LINE

At SANDSTONE, we don’t claim to know the future. That is why we are taking a tactical approach to the AI rollout where we have exposure to the builders, enablers and second-order beneficiaries that stand to gain if things go well but also have strong fundamental business models that will be required regardless of how the AI narrative plays out. Instead of chasing the biggest names and betting everything on one thesis, our positioning gives us the flexibility to proactively adjust to market conditions and remain in a strong stance no matter which way the wind blows.

Markets are uncertain. Your strategy shouldn't be.

Find confidence during confusing times by meeting with one of our wealth professionals.