The analogy likens central bankers increasing interest rates to fishermen throwing dynamite into the ocean. When the dynamite explodes, little fish rise to the surface quickly, but the larger impacts are not immediately noticeable as they take longer to rise to the surface. The fishermen do not immediately see the whales, so they keep tossing in dynamite until it is too late and are forced to reevaluate their method of fishing. So, with the steady stream of dynamite coming from central banks for over a year and a half, what have been the quick-to-rise fish, and what is the whale heading for the surface?

The Little Fish Rise First

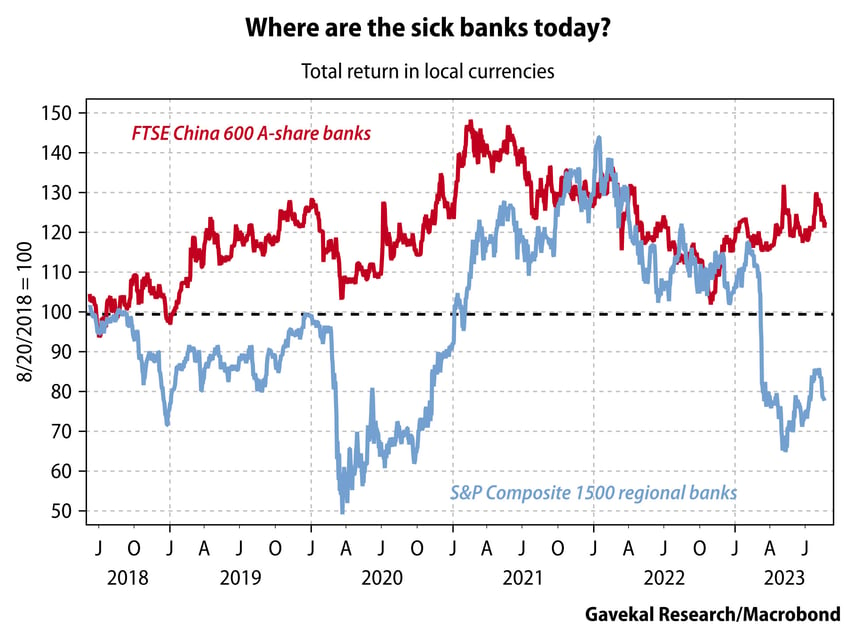

In the whale-spotting analogy, the smaller fish tend to be interest rate-sensitive firms such as commercial banks. Commercial banks are vital to spurring growth in the economy through lending, making their performance a leading indicator of both the economy and asset prices. With the continued media focus on a Chinese economic collapse, one would expect their bank shares to have experienced a meltdown, though this has not been the case. Instead, US regional banks are the ones heralding a meltdown after collectively experiencing two major selloffs over the last five years. The information we receive from business media and from markets has never been more different, and looking beyond cover stories to what markets are saying is more important than ever. China’s slowing growth is concerning, but it should not be used as a diversion from the larger story unfolding in the US.

The Whale Beneath the Surface – The US Treasury Meltdown

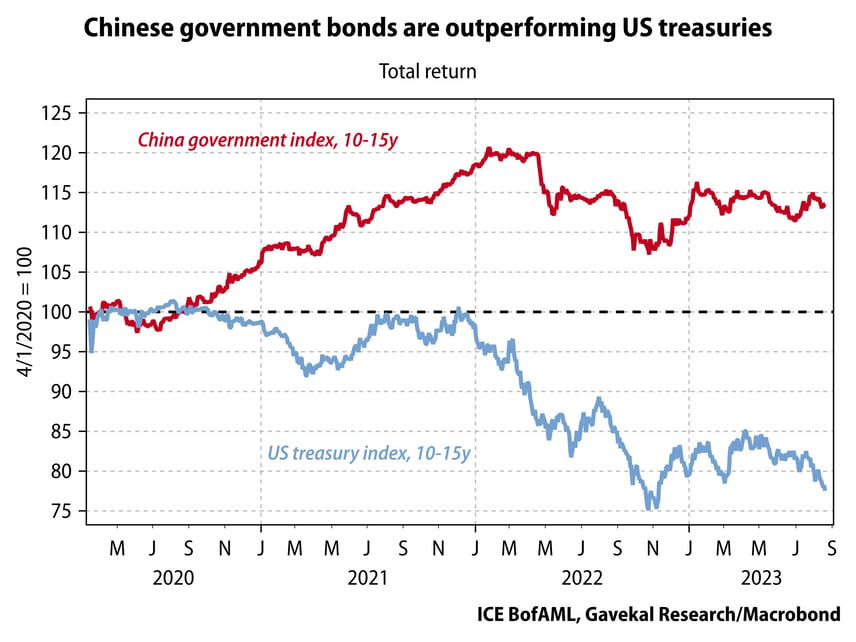

Generally, government bonds are viewed as a safe-haven asset meant to lower the volatility of a portfolio. When uncertainty increases, there is a flight to safety that involves investors rushing to purchase government bonds. This drives their prices higher and, inversely, decreases their yields. With the media’s focus on rising recession risks out of Europe and China, investors would be expected to rush into US Treasuries. Instead, what we have seen over the past month and, to an extent, over the last few years is a puzzling divergence. Chinese bonds have significantly outperformed their US counterparts, and this month, US yields were driven to highs not seen since the Great Financial Crisis. We believe that higher US Treasury yields may be the whale that is beginning to breach the surface, but this raises some questions. Why have investors soured on what was once the world’s safest asset?

The Resurgence of Latin Bonds

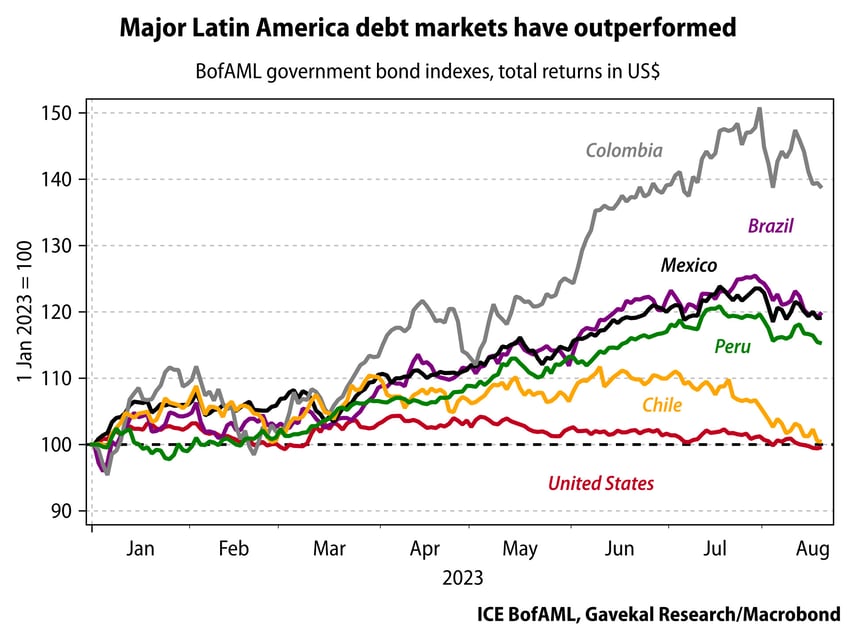

One explanation could be that Latin American countries have become far more prudent in managing their finances. Fiscal and monetary policies over the last few years across Latin America have been much more conservative when compared to Western governments. Their central banks moved to counteract inflation much faster than most, and that has allowed them to consider lowering interest rates while other countries are still considering hikes. Government debt markets for countries like Brazil, Mexico, and Colombia have also vastly outperformed US government bonds since the start of this year, lending some support to the idea that maybe the US Treasury is not the only government bond worth owning anymore.

A Weakening Financial Footing

The second explanation for investors not rushing into the Treasury market is that they may be recognizing that the US is on its weakest financial footing in decades. A credit rating downgrade, a near-government default, regional banking difficulties, and exponentially rising interest costs may finally be weighing on investor sentiment. Since the Great Financial Crisis, government debt has grown much more quickly than the economy, though the budgetary impacts were minimal as interest rates were at record lows. Today, that debt is no longer as cheap, and the US is starting to look overleveraged to the point that it may have to look at raising taxes, trimming spending, or leaning on the Federal Reserve to lower rates at the expense of the US dollar.

BOTTOM LINE

This year, the small fish received all the media attention, but the meltdown in the US Treasury may be the whale that is just hiding beneath the surface. For the first time, we are seeing investors shy away from the traditional bedrock that is the US Treasury, and the implications for the economy, fiscal and monetary policy, and currencies are immense.